For South African investors, the past few years have been extremely trying. The only asset class that has delivered annualised returns of more than 10% over this period is local bonds.

Both local and international equities have performed below inflation, global bonds have only barely produced a positive return in rand terms, and the local listed property has been negative. As Claire Rentzke, chief investment officer of 27four Investment Managers, puts it, there has been nowhere to hide.

“Over this three-year time horizon we have continued to get very low returns from the market,” she says. “It has been very difficult to generate inflation-beating returns from the asset classes that we have available.”

Investors have also had to stomach these poor returns in a broader environment that is highly uncertain due to what is happening on the geopolitical front. The challenges at state-owned enterprises, weak government finances, the country facing an election year, and ongoing revelations about the scale of corruption being uncovered by the Zondo Commission are making South Africans understandably nervous.

“On the back of all this we have also seen earnings and trading updates from companies that show what a tough environment it is at the moment, particularly for the local retailers,” Rentzke says. “Consumers have far less income to spend.”

Blood on the JSE

All of this has compounded on the local market, with 2018 being the first year in a decade that the FTSE/JSE All Share Index (Alsi) ended in negative territory. This weakness was also very widespread, with more than 60% of the companies in the index being down for the 12 months to the end of December.

This is only the third time in the last 20 years that there has been such broad market negativity. The first was in 1998 following the Asian crisis, and the second was the global financial crisis of 2008.

It is purely coincidental that these events are all exactly a decade apart, but what may be less so is what followed on each occasion. As the following chart shows, subsequent to each of these years, the JSE rebounded strongly.

In 1999, the JSE recorded its highest annual return of the last 40 years at 61.4%. In 2009 the market bounced 32.1%.

“So if history is anything to go by, the broad-based sell-off we saw in equity markets in 2018 does present quite an interesting number of opportunities,” says Nadir Thokan, portfolio manager at 27four. “If you are looking at multiples, the JSE is trading at a forward price-to-earnings ratio of under 12 times, which is well below the five and 10-year averages.”

The shape of the market

Some investors however caution that the outlook for company profits is getting worse, as shown by some poor recent updates from retailers like Shoprite. The market is therefore purely adjusting to this lower earnings base.

Yet 27four’s analysis shows that earnings on the JSE are still growing. As the chart below shows, the overall earnings level on the JSE has increased 30% over the last two years.

It is true that resource companies have had a large impact on this figure as their earnings have recovered from a very low base. The picture may therefore not be quite as rosy as this chart indicates, but it is nevertheless true that earnings of listed companies are broadly holding up.

“The bottom line is that you are getting a growing stream of earnings for significantly lower prices today than you were in the last two years when the country was certainly in a recession,” says Thokan. “Even in these tough times, companies have pulled different levers to grow their earnings.”

What should also give investors something to consider is just how widespread the opportunity set on the local market now is from a valuation perspective. More than 60% of the stocks on the Alsi are trading at price-to-earnings multiples of lower than 14 times, which is the market’s long term average.

“That is the highest proportion of companies trading at below average multiples in the last five years, and comfortably so,” Thokan points out. “This talks to the depth of opportunities available. Surely within that 60% of the market, even if there are a significant number of value traps due to an inability to grow earnings, there must be a decent number of opportunities.”

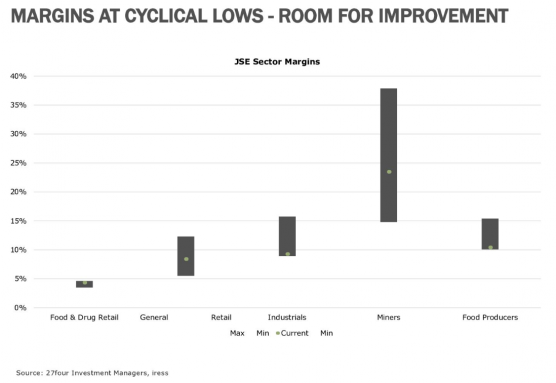

Coupled with this is that margins for listed companies across sectors are at cyclical lows. As the chart below shows, only food and drug retailers are securing margins near the top of their historical range. This is, however, a sector that always operates on thin margins, regardless of the environment.

“We have margins at a structural low, which makes them unlikely to go significantly lower, prices very depressed, and earnings that have held up okay,” says Thokan. “We think that the combination of these factors is presenting quite an interesting opportunity on the JSE. The risk is that multiples can still go lower in the short term due to poor investor sentiment, but the fact that we are trading at such a discount makes the likelihood of that happening less likely than a year ago.”

AUTHOR: Patrick Cairns

This article was originally posted at https://www.moneyweb.co.za/investing/can-things-still-get-worse-on-the-jse/